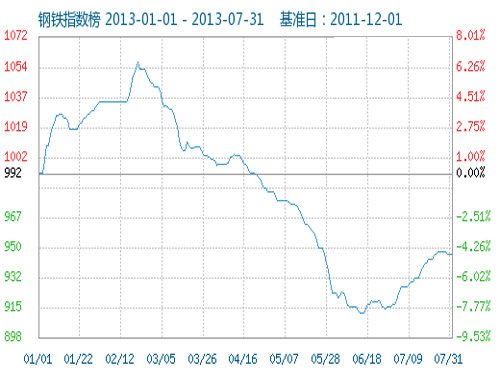

From the end of June to July, since the steel price changed its trend, it was in a contrarian upward trend, and there was a strong off-season market and the market was picking up. However, due to the shelving of downstream demand, the trading volume in the market was reduced, causing the steel market to have a market correction at the end of July, and steel prices fell slightly. . As of July 31, the business club’s steel index was 946 points, unchanged from the 30th, which was 10.50% lower than the highest point in the cycle of 1057 points (2013-02-21), and was higher than the lowest point of 827 points on September 09, 2012. 14.39%. (Note: Cycle refers to 2011-12-01 to date) Compared with June 27, the increase rate is 3.16%.

From the end of June to July, since the steel price changed its trend, it was in a contrarian upward trend, and there was a strong off-season market and the market was picking up. However, due to the shelving of downstream demand, the trading volume in the market was reduced, causing the steel market to have a market correction at the end of July, and steel prices fell slightly. . As of July 31, the business club’s steel index was 946 points, unchanged from the 30th, which was 10.50% lower than the highest point in the cycle of 1057 points (2013-02-21), and was higher than the lowest point of 827 points on September 09, 2012. 14.39%. (Note: Cycle refers to 2011-12-01 to date) Compared with June 27, the increase rate is 3.16%. Therefore, although the overall steel market in July was in a rally, and there was a downward trend at the end of the month, the decline was not expected to increase, and it was in a correction in the short-term. As of July 31, commodity data provider - Business Club (100ppi.com) released the July 2013 commodity supply and demand index BCI of -0.06, an average increase of 1.05%, reflecting that the manufacturing economy contracted from the previous month. State, the economic downside risk weakened. Among the eight sectors monitored by BCI, the largest increase was colored plates, which rose by 7.54%, followed by steel, which rose by 2.84%; the largest decrease was agricultural and sub-sectors, which fell by -1.51%; followed by building materials, which dropped by -0.91. %.

Iron Ore: Rising sluggish gains are slowing down in August The main adjustment since July is that iron ore was first affected by the speculation of iron ore prices in late June, leading to a sharp rise in domestic ore prices, with a 2.42% weekly rise. The steel mills' inventory consumption is close to a low level due to their own ore stocks, and there is a demand for restocking, which in turn raises the ore price again. However, due to the impact of steel costs and the market’s resistance to high ore prices, the increase in ore prices gradually narrows; at the end of the month, due to the Platts index. Instead, there has been a slight correction. Therefore, the iron ore market in July to the overall rise, showing upward trend of the ladder, until the end of the month's callback market.

In terms of prices, according to the price monitoring of business clubs, by the end of July 31, the average price of 62% of the printing ink ports rose from 847.5 yuan/ton on July 1 to 885 yuan/ton, with a cumulative increase of 4.42%; For 2.42%, 0.35%, 1.03%, and 0.28%, the movements in the upward and downward direction were “anti-N†type, and the rate of increase gradually weakened.

In terms of inventory, according to statistics from the business community, as of July 26, the number of iron ore inventories at the national port was 72.3 million tons, a cumulative decrease of approximately 1.29 million tons from 73.59 million tons on July 5. However, it increased by 64 compared to the previous week. Ten thousand tons. The trend of inventories is inversely correlated with their price trends. Inventory levels have fallen before they rise, which fully benefits the ore market.

In the market, the recent frequent tendering of mines artificially stimulated the “demand phenomenon†and the spot trading platform in Singapore was relatively active. However, the domestic iron ore spot platform still maintained a tepid market, only recently driven by the international external environment. , showing a rise in popularity over the previous month. In general, spot transactions have gradually weakened since July, and market prices have been falling.

Liao Gang, an ore analyst at Business Club, believes that in July ore market, due to the decline in downstream stocks, environmental protection and other factors of steel mills led to the billet price increases, making the mines use the spot platform and bidding methods, and gradually increase the market price, The steel mills were forced to raise steel prices to provide support for the rise in ore prices. The recent ore market is weak. The main reason is that the current steel mills have reduced the purchase of ore stocks due to the gradual reduction of steel sales; at the end of the month, the funding of steel mills is also a strain. As a result of negative factors, Lv Gang believes that the ore market in August is still dominated by the oscillation correction.

Iron ore - steel billets - steel industry chain: pull the whole body in August and the steel price correction mainly from the steel prices point of view, according to the business community price monitoring shows that in July 2013, commodity prices rose in the list of the steel sector There were a total of 13 commodities that had risen, of which 3 products had risen by more than 5%, accounting for 21.4% of the monitored commodities in this sector; the top 3 commodities for the increase were Panluo (6.40%) and Rebar (distribution) (5.97). %), wire (5.01%). There was a total of one commodity that fell month-on-month, and the drop was galvanized sheet (-0.08%). The average monthly price in July was 3.27%. The gains in the first four weeks were 1.19%, 0.51%, 0.85% and 0.38%, respectively. This is exactly the same as mine prices.

From the standpoint of billet price, although billet prices also show a ladder-like upward trend, the upward and downward movements show a “V†pattern, with market gains decreasing first and then rising. (According to the business community price monitoring, the first four weeks of gains are 3.03%, respectively. 1.31%, 0.64% and 0.97%); however, the market rebound rate of the billet in July is still high. Although last weekend (ie, July 27-28), the billet price in the Tangshan region had a 20 yuan/ton price correction, which has dampened market confidence; but overall, the July billet still dominated by rising prices. As of July 31, the ex-factory price of Tangshan billet tax included was 3,090 yuan/ton, which was 3.88% higher than that of July 1, and the tender price of Tangshan Yansteel billet was included at 3,100 yuan/ton on July 31st. Compared with the previous week, the price was 41 yuan/ton lower, and the ex-factory price of the current local steel mill was 10 yuan/ton higher and the acceptance price increase was 110 yuan/ton. The bid price for the second consecutive month fell. It is expected that the market outlook will be stable and the transactions will be general.

It can be seen that the iron ore-steel billet-steel industry chain's upstream and downstream price trends remain basically the same, and the market synchronicity is extremely high. The ups and downs will affect the whole body.

From the steel inventory point of view, according to statistics show business stocks, as of July 26, the five major steel stocks in major cities nationwide was 15.39 million tons, has been continuous decline for 19 weeks, a cumulative decrease of 7.125 million tons, the average weekly consumption stock At 374,300 tons, the overall decline was 32% compared with the week of March 15. The stocks of rebar and wire rods have also dropped continuously for 19 weeks, and the average number of declines in building materials per week is about 90% of the total. It can be seen that most of the consumption of steel stocks is building materials. The consumption of inventory; therefore, the demand for the construction steel market, such as real estate and infrastructure projects, has always been the focus of steel terminal demand since 2013. According to the statistics of the China Iron and Steel Association, the steel stocks of key steel mills are approaching the highest point in history.

According to data from the China Steel Association, as of July 26, the inventory of steel in 76 key steel enterprises was 12.45 million tons, which was an increase of 658,800 tons from 11.79 million tons in the first half of July, approaching the highest level in mid-February 2013. Inventory of 12.46 million tons. Although the decline in steel stocks in the steel industry is favorable for steel prices, the high stocks in steel mills have prevented steel prices from continuing to rise.

From the aspect of billet inventory, according to the statistics of the business community, as of July 26, the Tangshan warehouse port billet inventory of the same caliber was 565,000 tons, which was up 5,200 tons from the previous week. The stocks were up and down, and the market was bearish; At the end of July, Tangshan Yan Gang’s general bills were tendered for a total of 20,500 tons of tenders, including 10,000 tons of Jinxin, 2,000 tons of Xinshengsheng, 3,000 tons of Hebei Taigang, 3,000 tons of Xinyiyuan and 2,500 tons of Xiamen Haiyi. In general, although the stock consumption of slabs is slow, the demand for stockpiling by steel mills remains.

From the above data, it can be seen that the inventory of the iron ore-slab-steel industry chain is basically in a downward trend. For steel prices: The rising ore price of ore stocks fell, which favored steel prices; the decline in billet inventory prices also supported steel prices. Therefore, at the end of the month when the price of steel fell, the aforementioned good support would not result in a larger decline.

From the perspective of steel production, according to data calculated by China Iron and Steel Association, in the middle of July, China produced a total of 21.3302 million tons of crude steel, 19,345,400 tons of pig iron and 30.1462 million tons of steel. The average daily output was 2,130,300 tons of crude steel, 1,934,500 tons of pig iron and 3,104,600 tons of steel respectively. In July, the cumulative daily production was 2,086.9 thousand tons of crude steel, 1,918,500 tons of pig iron and 2,982,100 tons of steel, and in early July The average daily output of crude steel in the country had dropped to 2.083 million tons, which fell by 4.5% in the first half of the decade, setting a year-to-date decline in the year. This was the first time that the crude steel fell below 2.1 million tons since the beginning of April this year. The rise of crude steel production in mid-July has led to a further increase in steel supply to the market and a bearish steel price.

From the perspective of the price adjustment of steel mills, according to the price adjustment information of business clubs, as of July 30, there are 24 steel mills in the country adjusting their ex-factory prices. Among them, 18 steel mills adjusted the ex-factory price of construction steel, 4 steel mills adjusted the ex-factory price of plate, 3 steel mills adjusted ex-factory prices of cold and hot coils, 1 steel mill adjusted cold-draw drawing prices, 1 steel mill Adjust the strip price. Most of these are downward adjustments, and the overall price adjustment range is between 10-30, which is relatively small compared to the price increase in early July.

From the point of view of maintenance of steel mills, according to the inspection and repair information from business clubs, as of July 26, the number of steel mills inspected has been reduced. The overall impact on plate production is about 460,000 tons, and the production of hot metal is about 62 million tons, which is more than before. With an increase, the steel supply in the market has decreased, which has formed a support for steel prices.

According to data. As of July 26th, 20 steel mills in Tangshan had a total of 25 232mm or more strip lines, among which 19 strip lines were in normal production and 6 were overhauled, affecting a total output of 10.05 million tons. The operating rate was 76%, which was flat compared to the previous week. 21 steel mills have a total of 24 145mm strip lines, among which 11 strip lines are in normal production and 13 are overhauled, affecting 139,400 tons of output. The operating rate is 46%, down 8% from the previous week; the thickness of Beijing-Tianjin-Hebei area The output of board production enterprises totaled 227,500 tons, a decrease of 14,000 tons from the previous week; the utilization rate was 63.1%, a decrease of 3.9% from the previous week. As a result, the operating rate of steel mills in Hebei has decreased significantly compared with that before, and the local steel supply is slightly insufficient, supporting the formation of steel prices.

Therefore, in summary, the iron ore-steel billet-steel industry chain is still dominated by rising prices in July. However, due to the decline in social stocks, steel mills have high stocks; billet inventory declines, billet prices increase; steel mill operating rates decline, crude steel production rises; steel mills cut prices, repairs increase, etc. At the end of the month, there was a downward trend. However, compared with the previous gains, it was still in a correction, and the real decline has not yet arrived.

Terminal demand: sluggish shipbuilding industry dragged down the market Steel market shipbuilding industry is currently facing the challenge of changing the operating environment, and as the main upstream of the shipbuilding industry, the market demand for non-ferrous metals and steel products is plagued by difficulties.

In the first half of 2013, the performance of large shipbuilding companies was generally sluggish, and the decline was considerable. The operating revenue of China Shipbuilding Co., Ltd. was nearly 319 million yuan, a decrease of 39.49% from the same period of last year. The total profit of the company was -60.31 million yuan, which was directly a huge loss from the profit of 2.4171 million yuan in the same period last year. China Ship’s quarterly quarterly report stated that operating income was approximately 381 million yuan, a decrease of 38.95% year-on-year; net profit attributable to shareholders of listed companies was a year-on-year decrease of 73.08%. According to the Guangzhou Shipyard International Quarterly Report, operating income for the first quarter was approximately RMB910 million, a decrease of 50.86% from the same period of the previous year, while net profit was reduced by 33.10% year-on-year. China South Heavy Industries revised its semi-annual results announcement on July 11 and said that it expects this year to come 1- The net profit attributable to the shareholders of the listed company in June was 24,237,700 yuan -38,883,900 yuan, a decrease of 20% - 50% over the same period of the previous year; Rongsheng Heavy Industry Group - China's largest civilian-building ship company has been reduced due to falling orders. Forced production cuts and layoffs of more than 8,000 people, and following a huge loss of 573 million yuan last year, the renewal of losses in the first quarter was 49 million yuan.

In the report, listed shipbuilding companies often stated that the ship market continued to weaken and competition intensified, and the number and prices of related product orders fell sharply. Therefore, it is expected that the recovery of the domestic shipbuilding industry in 2013 will be far from attainable as the shipping market remains depressed.

Macroscopically: Steady economic growth and good long-term steel prices The Central Political Bureau of China proposed 10 measures to do the work in the second half of the year: It is necessary to grasp the direction, intensity, and rhythm of macroeconomic regulation and control so that economic operations are in a reasonable range. Continue to implement proactive fiscal policies and sound monetary policies; maintain reasonable investment growth, and promote stable and healthy development of the real estate market in the second half of the year.

The Politburo meeting, including Xinhua News Agency and other media, emphasized the bottom line thinking and emphasized that the economy will continue to maintain a reasonable rate of growth in the second half of the year. Special mention will be made to promote the steady and healthy development of the real estate market in the second half of the year. At the same time, the Director of the Statistics Department of the Central Bank wrote a special article. The rise in house prices has nothing to do with the money supply. These arguments are in line with the mild stimulus of the previous period, which means that the investment-led stimulus is in progress. Reflecting from the macroscopic side, steel prices still have room to rise.

In conclusion, He Hangsheng, a steel analyst at Business Club, believes that the steel market is currently in a precarious period, bearish factors dominate, and favorable factors are difficult to ignore. In the long and short intertwined game market, steel prices are as frightening, the market is slightly Change, there will be ups and downs. He Hangsheng believes that under the current market conditions, the steel price in August should be dominated by the downward trend of the oscillation. Although from the above favorable factors, the steel price increase factor still exists, but it will directly affect the rise in steel prices, but it still takes time. Japan, while the current policy decisions will be the key to determining the market for the second half of the steel market. Therefore, although the decline in steel prices in August was limited, the rise was weak.

We are manufacturer with fully completed Sliding Door Systems including Home Barn Door Hardware,Mini Barn Door Hardware,Heavy duty barn door hardware,Pocket door hardware and other barn door hardware products with more than 14 years of manufacturing . Our products are perfectly fit to residential home doors,commercial doors,farm doors and other outdoor using .

You may select the styles from our existing designs.Classically,simply and conveniently,we will make you own a cosy place.

We welcome DIY designs as well.Let us help you for a distinctive and own-style home.

Sliding Door Systems

Sliding Door Systems,Sliding Door Hardware,Heavy Duty Sliding Door Hardware,Industrial Sliding Door Hardware,Sliding Barn Door Kit

Foshan Nanhai Xin Jianwei Hardware Co., Ltd , http://www.aaghardware.com