Over the past few weeks, the steel market has seen a mix of developments. With winter setting in across the northern regions, shipments from the north have started impacting the supply dynamics in the southern markets. Long products have been particularly affected by seasonal changes, whereas the sheet metal segment has shown signs of gradual improvement, thanks to stabilization in the manufacturing sector. However, sheet metal prices have continued to climb, prompting观望情绪 (wait-and-see attitudes) among downstream users. It's anticipated that the domestic steel market will experience minor fluctuations and consolidation in the near term.

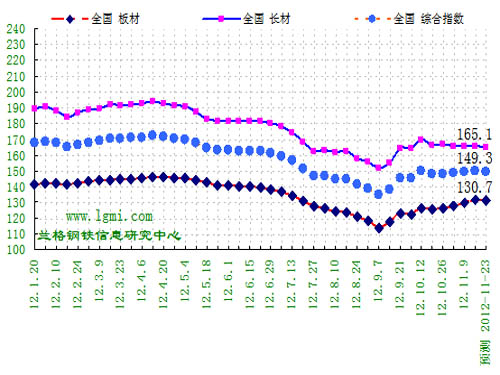

According to the Lange Steel Information Research Center’s weekly price forecasting model, domestic steel prices are expected to fluctuate this week (November 19-23). Long products are likely to see further declines, while plate market prices may experience both upward and downward movements. The composite Lange Steel Index is projected to hover around 149.3 points. The average steel price should remain around 3,880 yuan, with fluctuations of approximately 20-30 yuan. The long product index is expected to fluctuate around 165.1 points, dropping slightly by about 0.3 points. Meanwhile, the plate index is expected to fluctuate around 130.7 points, with a minor adjustment of around 0.7 points.

A survey conducted by the Lange Steel Information Research Center suggests that domestic long product prices will continue to decline this week, while plate market prices will show mixed trends. Raw material prices are also expected to vary, with iron ore prices declining steadily by 10 yuan, coke prices rising slightly by 20-30 yuan, scrap prices falling by 50 yuan, and billet prices decreasing slightly by 10-30 yuan.

In week 46 of 2012 (November 12-16), the Lange Steel (LGMI) Composite Price Index stood at 150.0 points, marking a week-on-week increase of 0.28% and a year-on-year decrease of 13.73%. The long product price index was 165.4 points, down 0.38% from the previous week and 16.77% lower than the same period last year. The plate price index was 131.4 points, up 1.29% week-on-week but down 8.67% year-on-year. Prices of major steel products monitored by the Lange Steel Information Research Center fluctuated slightly, with more varieties experiencing price increases compared to last week. Flat varieties saw minor decreases, while the number of falling varieties significantly increased. Out of 44 standard varieties, 14 showed price increases, 9 remained unchanged, and 21 experienced price drops. The domestic steel raw materials market showed mixed trends, with stable iron ore prices, a rise in coke prices by 30-70 yuan, mixed scrap prices, and a decline in billet prices by 40-80 yuan.

National steel social inventories continued their decline for the fifth consecutive week, with a slightly accelerated pace of reduction. Building materials inventory levels dropped more rapidly, while the rate of decline in plate inventories also picked up. As of November 16, steel social inventories in 29 key cities across the country stood at 11.6949 million tons, down 314,700 tons from the previous week. Wire rod inventories were 968,100 tons, down 3.61% from the prior week. Reinforced bar inventories were 4,436,000 tons, down 1.91% from last week. Coiled steel inventories were 261,700 tons, down 1.06% from the previous week. Hot-rolled coil inventories were 3.3342 million tons, down 3.26% from the previous week. Cold-rolled coil inventories were 1.5615 million tons, down 1.54% from the previous week. Plate inventories were 1,955,500 tons, down 3.61% from the prior week.

In week 46 of 2012 (November 12-16), the rebar market experienced turbulence and consolidation, with the overall price center gradually moving upward. The closing price this week was three points higher than the previous week. The market remains in a slow upward trend. The main contract volume this week was 1.003 million contracts, down 671.32 million lots. Outflows in lightening warehouse receipts were primarily due to short selling positions.

Recent macroeconomic indicators have provided some insights into the factors influencing steel prices. Industrial added value for enterprises above designated size increased by 9.6% year-on-year in October, up 0.4 percentage points from September. Fixed asset investment from January to October increased by 20.7% year-on-year, showing a slight acceleration compared to the first nine months. M2 money supply at the end of October was 14.1% higher year-on-year, down 0.7 percentage points from the previous month.

In terms of raw material supply, iron ore imports fell sharply in October, totaling 64.43 million tons, down 8.58 million tons from the previous month. The average price of imported iron ore was $104.9/ton, down $11 from September. Steel exports in October were 4.84 million tons, down slightly from September but up 26.7% year-on-year. Imports were 1.03 million tons, down 170,000 tons from September and 14.2% lower year-on-year.

Looking ahead, regulatory measures such as the comprehensive steel industry emission reduction plan in Shandong Province aim to reduce carbon emissions in the steel sector by 47.4% by 2015. Additionally, the EU’s anti-dumping investigations into Chinese steel products highlight ongoing global trade tensions.

Overall, the steel market remains cautious, with both bullish and bearish factors at play. While some sectors like real estate and automotive show signs of recovery, broader economic uncertainties could impact demand and pricing dynamics in the coming weeks.

Over the past few weeks, the steel market has seen a mix of developments. With winter setting in across the northern regions, shipments from the north have started impacting the supply dynamics in the southern markets. Long products have been particularly affected by seasonal changes, whereas the sheet metal segment has shown signs of gradual improvement, thanks to stabilization in the manufacturing sector. However, sheet metal prices have continued to climb, prompting观望情绪 (wait-and-see attitudes) among downstream users. It's anticipated that the domestic steel market will experience minor fluctuations and consolidation in the near term.

According to the Lange Steel Information Research Center’s weekly price forecasting model, domestic steel prices are expected to fluctuate this week (November 19-23). Long products are likely to see further declines, while plate market prices may experience both upward and downward movements. The composite Lange Steel Index is projected to hover around 149.3 points. The average steel price should remain around 3,880 yuan, with fluctuations of approximately 20-30 yuan. The long product index is expected to fluctuate around 165.1 points, dropping slightly by about 0.3 points. Meanwhile, the plate index is expected to fluctuate around 130.7 points, with a minor adjustment of around 0.7 points.

A survey conducted by the Lange Steel Information Research Center suggests that domestic long product prices will continue to decline this week, while plate market prices will show mixed trends. Raw material prices are also expected to vary, with iron ore prices declining steadily by 10 yuan, coke prices rising slightly by 20-30 yuan, scrap prices falling by 50 yuan, and billet prices decreasing slightly by 10-30 yuan.

In week 46 of 2012 (November 12-16), the Lange Steel (LGMI) Composite Price Index stood at 150.0 points, marking a week-on-week increase of 0.28% and a year-on-year decrease of 13.73%. The long product price index was 165.4 points, down 0.38% from the previous week and 16.77% lower than the same period last year. The plate price index was 131.4 points, up 1.29% week-on-week but down 8.67% year-on-year. Prices of major steel products monitored by the Lange Steel Information Research Center fluctuated slightly, with more varieties experiencing price increases compared to last week. Flat varieties saw minor decreases, while the number of falling varieties significantly increased. Out of 44 standard varieties, 14 showed price increases, 9 remained unchanged, and 21 experienced price drops. The domestic steel raw materials market showed mixed trends, with stable iron ore prices, a rise in coke prices by 30-70 yuan, mixed scrap prices, and a decline in billet prices by 40-80 yuan.

National steel social inventories continued their decline for the fifth consecutive week, with a slightly accelerated pace of reduction. Building materials inventory levels dropped more rapidly, while the rate of decline in plate inventories also picked up. As of November 16, steel social inventories in 29 key cities across the country stood at 11.6949 million tons, down 314,700 tons from the previous week. Wire rod inventories were 968,100 tons, down 3.61% from the prior week. Reinforced bar inventories were 4,436,000 tons, down 1.91% from last week. Coiled steel inventories were 261,700 tons, down 1.06% from the previous week. Hot-rolled coil inventories were 3.3342 million tons, down 3.26% from the previous week. Cold-rolled coil inventories were 1.5615 million tons, down 1.54% from the previous week. Plate inventories were 1,955,500 tons, down 3.61% from the prior week.

In week 46 of 2012 (November 12-16), the rebar market experienced turbulence and consolidation, with the overall price center gradually moving upward. The closing price this week was three points higher than the previous week. The market remains in a slow upward trend. The main contract volume this week was 1.003 million contracts, down 671.32 million lots. Outflows in lightening warehouse receipts were primarily due to short selling positions.

Recent macroeconomic indicators have provided some insights into the factors influencing steel prices. Industrial added value for enterprises above designated size increased by 9.6% year-on-year in October, up 0.4 percentage points from September. Fixed asset investment from January to October increased by 20.7% year-on-year, showing a slight acceleration compared to the first nine months. M2 money supply at the end of October was 14.1% higher year-on-year, down 0.7 percentage points from the previous month.

In terms of raw material supply, iron ore imports fell sharply in October, totaling 64.43 million tons, down 8.58 million tons from the previous month. The average price of imported iron ore was $104.9/ton, down $11 from September. Steel exports in October were 4.84 million tons, down slightly from September but up 26.7% year-on-year. Imports were 1.03 million tons, down 170,000 tons from September and 14.2% lower year-on-year.

Looking ahead, regulatory measures such as the comprehensive steel industry emission reduction plan in Shandong Province aim to reduce carbon emissions in the steel sector by 47.4% by 2015. Additionally, the EU’s anti-dumping investigations into Chinese steel products highlight ongoing global trade tensions.

Overall, the steel market remains cautious, with both bullish and bearish factors at play. While some sectors like real estate and automotive show signs of recovery, broader economic uncertainties could impact demand and pricing dynamics in the coming weeks.

Single Function Hand Shower,Hand Shower In Bathroom,Hand Shower For Toilet,Gold Hand Shower

ASHOWER , https://www.ashower.com