With the gradual onset of winter in the northern parts of the country, the steel industry is entering its traditional demand lull. However, steel mills are resuming operations, and the cost support remains robust. While the long products market faces seasonal pressures, the sheet metal sector is experiencing a relatively stable manufacturing environment. Fortunately, short-term projections suggest that the domestic steel market may see slight fluctuations, with stronger performance anticipated for steel plates compared to long products.

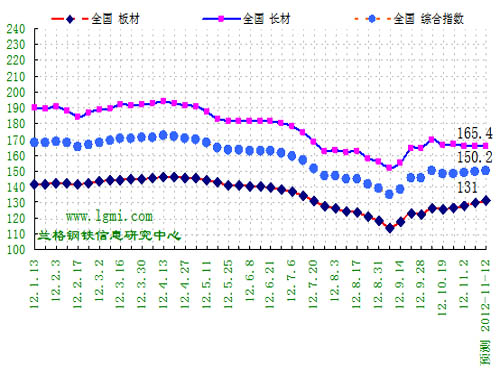

According to the weekly price forecasting model data from the Lange Steel Information Research Center, domestic steel market prices are expected to edge upward this week (November 12-16). Long products may experience a minor decline, while the plate market could stabilize with slight increases. The Lange Steel Composite Index is projected to hover around 150.2 points, with an average steel price of approximately 3900 yuan, fluctuating within a range of 20-30 yuan. The long product index is expected to fluctuate around 165.4 points, with a slight decrease of around 0.6 points; the steel plate index is expected to fluctuate around 131.0 points, increasing slightly by around 1.2 points.

A market survey by the Lange Steel Information Research Center indicates that domestic long product prices might dip slightly this week, while steel plate prices could remain steady or rise slightly. Raw material prices are likely to exhibit mixed movements, with iron ore and billet markets remaining stable. Coke prices are expected to rise marginally by 30-50 yuan, whereas scrap steel prices may decline steadily by around 100 yuan.

Last week, from November 5-9, which marked the 45th week of 2012, the Lange Steel (LGMI) Composite Price Index reached 149.6 points, marking a week-on-week increase of 0.72%. Year-over-year, it decreased by 13.20%. The long product price index stood at 166.0 points, registering a week-on-week increase of 0.03%, but a year-over-year decrease of 15.31%. Meanwhile, the sheet price index was 129.8 points, up 1.80% week-on-week, but down 9.75% year-over-year.

According to price data from 44 standard varieties across 17 categories monitored by the Lange Steel Information Research Center, the market prices of major steel products showed slight fluctuations in the 45th week of 2012. Compared to the previous week, there were more varieties that saw slight increases than decreases. Out of 44 varieties, 17 rose, four declined, 14 remained flat, and three more varieties were flat compared to the prior week. Domestic iron and steel raw materials exhibited mixed price trends, with iron ore and scrap markets remaining stable, coke prices rising by 70-150 yuan, and billet prices dropping by 10-30 yuan.

This week, the national steel stock market experienced a slower decline. Overall, the national steel inventory has been consistently decreasing. The decline in building materials inventory has slowed slightly, while the reduction in sheet stocks accelerated somewhat. Market monitoring by the Lange Steel Information Research Center shows that as of November 9, total steel social stocks in 29 key cities nationwide stood at 12,279,500 tons, a decrease of 217,900 tons from the previous week. By subcategory, wire rod social inventories were 1,004,300 tons, down 2.29% from the previous week; rebar social inventories were 4,522,300 tons, up 0.12% week-on-week; panluo social inventory was 264,500 tons, down 6.04% from the previous week; hot-rolled coil social inventory was 3,454,800 tons, down 3.95% week-on-week; cold-rolled coil social inventory was 1,585,900 tons, down 0.72% week-on-week; and plate social inventory was 1,447,800 tons, down 1.89% week-on-week.

This week, the steel market remained volatile within a narrow range. In the 45th week of 2012, rebar and ferrous alloy markets oscillated narrowly, with the market's weakness becoming increasingly apparent. The settlement price fell by 36 points, but in reality, compared to the settlement price, it was only 5 points lower than the previous week, staying within a stable price range. This week, the main contract volume was 1.07 million contracts, an increase of 123,000 contracts. The 1305 contract continued to expand for two consecutive weeks, indicating growing enthusiasm for thread trading and foreshadowing the emergence of some medium-level prices.

Recent macroeconomic factors impacting steel prices include the rise in the non-manufacturing PMI by 1.8 percentage points in October. Additionally, the national consumer price index rose by 1.7% year-over-year, while the industrial producer's factory price fell by 2.8% year-over-year. National fixed asset investment increased by 20.7% year-on-year from January to October. The industrial added value above designated size increased by 9.6% year-over-year in October.

Industry news includes Shandong's steel industry restructuring, aiming to reduce steel enterprises from 21 to six major corporations by 2015. Crude steel production fell by 5.4% in the last quarter of October. The Ministry of Commerce has imposed anti-dumping duties on imports of certain high-performance stainless steel seamless pipes from the EU and Japan. Railway investments in fixed assets decreased by 0.9% year-over-year in October. Real estate development investment increased by 15.4% year-over-year, and national home appliance sales to rural areas exceeded 60 million units from January to October.

With the gradual onset of winter in the northern parts of the country, the steel industry is entering its traditional demand lull. However, steel mills are resuming operations, and the cost support remains robust. While the long products market faces seasonal pressures, the sheet metal sector is experiencing a relatively stable manufacturing environment. Fortunately, short-term projections suggest that the domestic steel market may see slight fluctuations, with stronger performance anticipated for steel plates compared to long products.

According to the weekly price forecasting model data from the Lange Steel Information Research Center, domestic steel market prices are expected to edge upward this week (November 12-16). Long products may experience a minor decline, while the plate market could stabilize with slight increases. The Lange Steel Composite Index is projected to hover around 150.2 points, with an average steel price of approximately 3900 yuan, fluctuating within a range of 20-30 yuan. The long product index is expected to fluctuate around 165.4 points, with a slight decrease of around 0.6 points; the steel plate index is expected to fluctuate around 131.0 points, increasing slightly by around 1.2 points.

A market survey by the Lange Steel Information Research Center indicates that domestic long product prices might dip slightly this week, while steel plate prices could remain steady or rise slightly. Raw material prices are likely to exhibit mixed movements, with iron ore and billet markets remaining stable. Coke prices are expected to rise marginally by 30-50 yuan, whereas scrap steel prices may decline steadily by around 100 yuan.

Last week, from November 5-9, which marked the 45th week of 2012, the Lange Steel (LGMI) Composite Price Index reached 149.6 points, marking a week-on-week increase of 0.72%. Year-over-year, it decreased by 13.20%. The long product price index stood at 166.0 points, registering a week-on-week increase of 0.03%, but a year-over-year decrease of 15.31%. Meanwhile, the sheet price index was 129.8 points, up 1.80% week-on-week, but down 9.75% year-over-year.

According to price data from 44 standard varieties across 17 categories monitored by the Lange Steel Information Research Center, the market prices of major steel products showed slight fluctuations in the 45th week of 2012. Compared to the previous week, there were more varieties that saw slight increases than decreases. Out of 44 varieties, 17 rose, four declined, 14 remained flat, and three more varieties were flat compared to the prior week. Domestic iron and steel raw materials exhibited mixed price trends, with iron ore and scrap markets remaining stable, coke prices rising by 70-150 yuan, and billet prices dropping by 10-30 yuan.

This week, the national steel stock market experienced a slower decline. Overall, the national steel inventory has been consistently decreasing. The decline in building materials inventory has slowed slightly, while the reduction in sheet stocks accelerated somewhat. Market monitoring by the Lange Steel Information Research Center shows that as of November 9, total steel social stocks in 29 key cities nationwide stood at 12,279,500 tons, a decrease of 217,900 tons from the previous week. By subcategory, wire rod social inventories were 1,004,300 tons, down 2.29% from the previous week; rebar social inventories were 4,522,300 tons, up 0.12% week-on-week; panluo social inventory was 264,500 tons, down 6.04% from the previous week; hot-rolled coil social inventory was 3,454,800 tons, down 3.95% week-on-week; cold-rolled coil social inventory was 1,585,900 tons, down 0.72% week-on-week; and plate social inventory was 1,447,800 tons, down 1.89% week-on-week.

This week, the steel market remained volatile within a narrow range. In the 45th week of 2012, rebar and ferrous alloy markets oscillated narrowly, with the market's weakness becoming increasingly apparent. The settlement price fell by 36 points, but in reality, compared to the settlement price, it was only 5 points lower than the previous week, staying within a stable price range. This week, the main contract volume was 1.07 million contracts, an increase of 123,000 contracts. The 1305 contract continued to expand for two consecutive weeks, indicating growing enthusiasm for thread trading and foreshadowing the emergence of some medium-level prices.

Recent macroeconomic factors impacting steel prices include the rise in the non-manufacturing PMI by 1.8 percentage points in October. Additionally, the national consumer price index rose by 1.7% year-over-year, while the industrial producer's factory price fell by 2.8% year-over-year. National fixed asset investment increased by 20.7% year-on-year from January to October. The industrial added value above designated size increased by 9.6% year-over-year in October.

Industry news includes Shandong's steel industry restructuring, aiming to reduce steel enterprises from 21 to six major corporations by 2015. Crude steel production fell by 5.4% in the last quarter of October. The Ministry of Commerce has imposed anti-dumping duties on imports of certain high-performance stainless steel seamless pipes from the EU and Japan. Railway investments in fixed assets decreased by 0.9% year-over-year in October. Real estate development investment increased by 15.4% year-over-year, and national home appliance sales to rural areas exceeded 60 million units from January to October.

Diesel Engine Fan Blades,Cooling Fan Blades,Axial Cooling Fan Parts,Engine Cooling Fan

Changzhou Keyleader Fan Technology Co. Ltd. , https://www.keyleaderfan.com