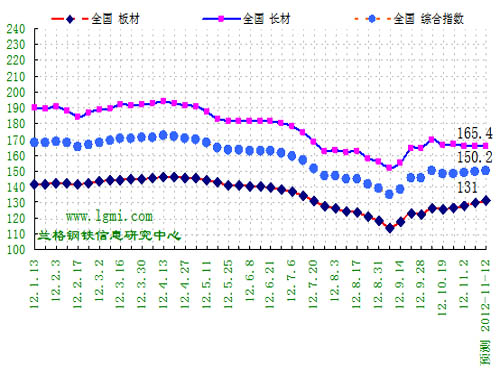

As winter approaches in the northern regions, the demand for steel products is likely to slow down due to seasonal factors. However, steel mills are gradually resuming operations, which could provide some cost support to the market. While long products continue to face seasonal pressures, the sheet metal sector is becoming more stable amid a favorable manufacturing environment. Fortunately, the domestic steel market is anticipated to remain relatively stable in the short term, with stronger performance in the plate sector and softer conditions for long products.

According to the weekly price forecast model data from the Lange Steel Information Research Center, domestic steel market prices are expected to edge upward this week (November 12-16), with long products markets experiencing a slight decline, while the plate sector is projected to remain steady with a slight increase. The Lange Steel Composite Index is forecasted to hover around 150.2 points, with the average steel price staying near 3900 yuan, fluctuating within a range of approximately 20-30 yuan. The Lange Steel Long Products Index is expected to fluctuate around 165.4 points, marking a modest drop of around 0.6 points; meanwhile, the Lange Steel Plate Index is anticipated to hover around 131.0 points, seeing a slight rise of approximately 1.2 points.

Based on the market survey conducted by the Lange Steel Information Research Center, domestic long products markets are predicted to see a minor downturn this week (November 12-16), whereas the plate sector is expected to stay relatively stable with a slight uptick. Raw material market prices may experience some variation, with iron ore and billet prices remaining largely stable. Coke prices are projected to increase slightly by 30-50 yuan, while the market price for scrap steel is anticipated to decline steadily by around 100 yuan.

1. Domestic steel market prices saw a slight increase during the 45th week of 2012 (November 5-9). The Lange Steel (LGMI) Composite Price Index reached 149.6 points, representing a week-on-week increase of 0.72% and a year-on-year decrease of 13.20%. The LGMI Long Products Price Index stood at 166.0 points, marking a week-on-week increase of 0.03% and a year-on-year decrease of 15.31%. Meanwhile, the LGMI Sheet Price Index was 129.8 points, registering a week-on-week increase of 1.80% and a year-on-year decrease of 9.75%.

Data from the Lange Steel Information Research Center shows that the market prices of major steel products fluctuated slightly in the 45th week of 2012 (November 5-9). Compared to the previous week, there was a marginal increase in the number of rising varieties among standard products, while the number of falling varieties slightly decreased. Out of 44 monitored standard varieties across 17 categories in certain regions, 17 varieties increased, four decreased compared to the prior week; 14 varieties remained flat, increasing by one compared to the previous week; 13 varieties decreased, increasing by three compared to the previous week. Domestic iron and steel raw materials experienced mixed price movements, with iron ore and scrap markets remaining stable, coke prices rising by 70-150 yuan, and billet prices declining by 10-30 yuan.

2. The national steel stock market showed a slower decline this week. Nationwide steel inventories have been continuously decreasing, though the pace of decline for building materials slowed slightly, while the decline in sheet stocks accelerated somewhat. According to market monitoring by the Lange Steel Information Research Center, as of November 9th, the total steel society inventory in 29 key cities nationwide was 12,279,500 tons, a decrease of 217,900 tons from the previous week. By sub-category, national wire rod social inventories stood at 1,004,300 tons, down 2.29% from the previous week; rebar social inventories were 4,522,300 tons, up 0.12% from the previous week; Panluo social inventory was 264,500 tons, down 6.04% from the previous week; hot-rolled coil social inventory was 3,454,800 tons, down 3.95% from the previous week; cold-rolled coil social inventory was 1,585,900 tons, down 0.72% from the previous week; and plate social inventory was 1,447,800 tons, down 1.89% from the previous week.

3. The steel market remained volatile within a narrow range this week. In the 45th week of 2012 (November 5-9), the rebar and ferrous alloy markets experienced limited fluctuations, with market sentiment becoming increasingly cautious. The settlement price for the week fell by 36 points, yet in reality, the settlement price this week was only 5 points lower than the previous week, essentially remaining within the same price range. This week, the total open interest for the main contract was 1.07 million contracts, an increase of 123,000 contracts. The 1305 contract continued to expand for two consecutive weeks, indicating growing enthusiasm for thread futures, which also hinted at the potential emergence of medium-level prices.

4. Recent macroeconomic factors influencing steel prices:

In October, the non-manufacturing PMI rose by 1.8 percentage points. Data released by the National Bureau of Statistics Service Survey Center and the China Federation of Logistics and Purchasing on November 3rd showed that China's non-manufacturing business activity index reached 55.5% in October, up 1.8 percentage points from the previous quarter. Additionally, the new orders and employment indices remained stable, while the business activity expectations index surged significantly, reaching 63.4%. These figures indicate a positive trend in the non-manufacturing sector with accelerating growth.

The overall consumer price level increased by 1.7% year-on-year in October. Urban areas saw a 1.8% increase, while rural areas experienced a 1.5% rise. Food prices climbed by 1.8%, and non-food prices increased by 1.7%. Consumer goods prices went up by 1.5%, and service prices rose by 2.3%. From January to October, the cumulative consumer price level increased by 2.7% year-on-year. In October, the consumer price level dropped by 0.1% compared to the previous quarter. Cities experienced a 0.1% drop, while rural areas also saw a 0.1% decrease. Food prices fell by 0.8%, while non-food prices rose by 0.3%. Consumer goods prices declined by 0.2%, whereas service prices increased by 0.2%.

The national industrial producer's factory price fell by 2.8% year-on-year in October. Data from the National Bureau of Statistics showed that industrial producer prices fell by 2.8% year-on-year and 0.2% month-on-month. Industrial producer purchase prices decreased by 3.3% year-on-year and rose by 0.1% month-on-month. From January to October, industrial producer ex-factory prices fell by 1.6% year-on-year, and purchase prices decreased by 1.7% year-on-year. Within ex-factory prices, the means of production fell by 3.7% year-on-year, including a 6.4% drop in mining industry prices, a 3.4% decline in raw material industry prices, and a 3.5% fall in processing industry prices. Living materials prices rose by 0.2% year-on-year, with food prices increasing by 0.3%, clothing by 1.6%, general commodities by 0.5%, and durable consumer goods falling by 1.0%. Among purchase prices, ferrous materials fell by 11.4% year-on-year, chemical raw materials by 5.7%, non-ferrous metal materials and wires by 3.1%, textile raw materials by 2.2%, and fuel power by 1.5%.

Fixed asset investment grew by 20.7% year-on-year from January to October. Data from the National Bureau of Statistics indicated that fixed asset investment (excluding rural households) reached 29,254.2 billion yuan from January to October, representing a nominal year-on-year increase of 20.7%, 0.2 percentage points higher than the growth rate for the first nine months. On a month-to-month basis, fixed asset investment (excluding rural households) increased by 1.94% in October.

By sub-sector, from January to October, investment in the primary industry was 743.7 billion yuan, up 32.3% year-on-year, 0.1 percentage points higher than the growth rate for the first nine months; investment in the secondary industry was 1,287.5 billion yuan, up 21.9%, 0.5 percentage points lower than the growth rate for the first nine months; investment in the tertiary industry reached 15,631.9 billion yuan, up 20.1%, 0.7 percentage points higher than the growth rate for the first nine months. Within the secondary industry, industrial investment was 1,258.3 billion yuan, up 21.9%, 0.6 percentage points lower than the growth rate for the first nine months. Among these, mining industry investment was 1,005.7 billion yuan, up 14.7%, 2.7 percentage points lower than the growth rate for the first nine months; manufacturing investment was 1,018.8 billion yuan, up 23.1%, 0.4 percentage points lower than the growth rate for the first nine months; investment in electricity, heat, gas, and water production and supply was 1,343.7 billion yuan, up 18.6%, 0.5 percentage points lower than the growth rate for the first nine months.

Industrial added value above designated size increased by 9.6% year-on-year in October. Data from the National Bureau of Statistics showed that industrial enterprises above designated size registered a year-on-year increase of 9.6% in their added value in October (the growth rate excluding price factors), which was 0.4 percentage points faster than in September. On a month-to-month basis, the added value of industries above designated size increased by 0.81% from the previous month in October. From January to October, the industrial added value of above-scale industries increased by 10.0% year-on-year.

By sub-sector, in October, the added value of all 41 major industrial sectors increased year-on-year. Textile industry growth was 11.9%, chemical raw materials and chemical products manufacturing growth was 11.9%, non-metallic mineral products industry growth was 11.0%, ferrous metal smelting and rolling processing industry growth was 12.6%, general equipment manufacturing industry growth was 7.1%, automobile manufacturing industry growth was 5.9%, railway, ship, aerospace, and other transportation equipment manufacturing growth was 6.1%, electrical machinery and equipment manufacturing growth was 7.9%, computer, communication, and other electronic equipment manufacturing growth was 10.1%, and electricity and heat production and supply industry growth was 4.7%.

Industry news:

Shandong Province is restructuring its steel industry by consolidating steel companies into six major groups by 2015. As a pilot region for structural adjustments in the steel industry, Shandong plans to reduce the number of steel enterprises from 21 to six major steel groups by 2015. Total steel production capacity will be adjusted from the current 63.07 million tons to 50 million tons, with an increase in coastal steel production to 43%. Enterprise mergers and acquisitions are a critical component of Shandong's steel structure adjustment pilot. On November 1st, the "Shandong Iron & Steel (Group) Co., Ltd. Merger and Reorganization Plan" was published. In addition to the core Shandong Steel Group, five regional steel enterprise groups will also be established in Zibo, Weifang, Laiwu, Linyi, and Binzhou.

Crude steel production fell by 5.4% in the last quarter of October. Statistics from the China Iron and Steel Association showed that the average daily output of crude steel for major and medium-sized enterprises in late October was 15.195 million tons, a decrease of 86,600 tons from the previous month and a 5.4% decrease from the previous month. In the second half of October, the country's crude steel production was estimated to be 21.183 million tons, with an average daily output of 1.926 million tons, a decrease of 73,000 tons from the middle of the month and a 3.7% decrease from the previous month. The data also showed that the average daily output of crude steel in October was 1.658 million tons, an increase of 1.4% from September.

The Ministry of Commerce decided to impose anti-dumping duties on imports of certain high-performance stainless steel seamless pipes originating from the European Union and Japan. On November 8th, the Ministry of Commerce issued Bulletin No. 72 of 2012, announcing the final results of the anti-dumping investigation into certain high-performance stainless steel seamless pipes. Starting November 9, 2012, anti-dumping duties of 9.2% to 14.4% will be imposed on imports of these products originating from the EU and Japan, valid for five years. After investigation, the investigating authority concluded that during the investigation period, there was dumping of the product under investigation, causing substantial damage to the relevant high-performance stainless steel seamless pipe industry in China, with a causal link between dumping and substantial damage. Therefore, the Ministry of Commerce decided to impose anti-dumping duties on the above products originating from the EU and Japan starting November 9, 2012. The Ministry of Commerce initiated an anti-dumping investigation into the aforementioned products on September 8, 2011, and issued a preliminary ruling on May 8, 2012, confirming the existence of dumping in the investigated products.

The rebar main contract for the 9th session closed up, with the main contract rising by 0.52%. The rebar main 1305 contract opened at 3,640 yuan/ton on the morning of the 9th, showing an intraday downward trend throughout the day. The lowest price of the day was 3,628 yuan/ton, and the highest was 3,673 yuan/ton, closing at 3,640 yuan/ton. The settlement price on the previous trading day (8th) rose by 19 yuan/ton, with a trading volume of 2,328,602 lots and open interest totaling 1,070,130 contracts, an increase of 10,862 contracts.

Downstream demand:

Fixed asset investment in railways decreased by 0.9% month-on-month in October. Statistics from the Ministry of Railways showed that from January to October, national railway fixed asset investment totaled 425.169 billion yuan, a year-on-year decrease of 0.9%. Among these, national railway infrastructure investment reached 361.816 billion yuan, a year-on-year decrease of 1.5%.

Statistics from the Ministry of Housing and Urban Development showed that from January to October, a total of 7.22 million sets of new urban housing security projects were completed, with approximately 505 million units finished, and an investment of 1,080 billion yuan was completed. According to the plan, this year, more than 7 million sets of urban housing projects will be newly built in cities, with approximately 5 million units planned for completion.

From January to October, national sales of home appliances to rural areas exceeded 60 million units. Statistics from the Ministry of Commerce showed that from January to October, 65.22 million units of home appliances were sold nationwide (excluding Shandong, Henan, Sichuan, and Qingdao), achieving sales of 175.24 billion yuan, representing year-on-year increases of 23.5% and 18.8%, respectively. In October alone, the country sold 7.91 million home appliances to rural areas, achieving sales of 21.38 billion yuan, representing year-on-year increases of 27.5% and 26.0%. As of the end of October 2012, the country had sold 283 million home appliances to rural areas, achieving sales of 681.1 billion yuan.

From January to October, national real estate development investment increased by 15.4% year-on-year. Data from the National Bureau of Statistics showed that from January to October, total real estate development investment in the country reached 5,769,900 million yuan, an increase of 15.4% year-on-year, the same growth rate as from January to September. Among these, residential investment was 3,974.0 billion yuan, an increase of 10.8%, with a growth rate increase of 0.3 percentage points, accounting for 68.9% of total real estate development investment.

From January to October, the housing construction area of real estate development enterprises was 538.149 million square meters, an increase of 13.3% year-on-year, with a growth rate 0.7 percentage points lower than that of the first nine months. Among these, the residential construction area was 403.203 million square meters, an increase of 10.9%. The area of new housing starts was 1,476.92 million square meters, a decrease of 8.5%, with a decline 0.1 percentage points narrower than that of January to September. Among these, the newly started residential area was 1,083.96 million square meters, a decrease of 12.7%. The completed building area was 58.317 million square meters, an increase of 17.3%, with a growth rate increase of 0.9%. Among these, the residential building completed area was 476.92 million square meters, an increase of 17.1%.

As winter approaches in the northern regions, the demand for steel products is likely to slow down due to seasonal factors. However, steel mills are gradually resuming operations, which could provide some cost support to the market. While long products continue to face seasonal pressures, the sheet metal sector is becoming more stable amid a favorable manufacturing environment. Fortunately, the domestic steel market is anticipated to remain relatively stable in the short term, with stronger performance in the plate sector and softer conditions for long products.

According to the weekly price forecast model data from the Lange Steel Information Research Center, domestic steel market prices are expected to edge upward this week (November 12-16), with long products markets experiencing a slight decline, while the plate sector is projected to remain steady with a slight increase. The Lange Steel Composite Index is forecasted to hover around 150.2 points, with the average steel price staying near 3900 yuan, fluctuating within a range of approximately 20-30 yuan. The Lange Steel Long Products Index is expected to fluctuate around 165.4 points, marking a modest drop of around 0.6 points; meanwhile, the Lange Steel Plate Index is anticipated to hover around 131.0 points, seeing a slight rise of approximately 1.2 points.

Based on the market survey conducted by the Lange Steel Information Research Center, domestic long products markets are predicted to see a minor downturn this week (November 12-16), whereas the plate sector is expected to stay relatively stable with a slight uptick. Raw material market prices may experience some variation, with iron ore and billet prices remaining largely stable. Coke prices are projected to increase slightly by 30-50 yuan, while the market price for scrap steel is anticipated to decline steadily by around 100 yuan.

1. Domestic steel market prices saw a slight increase during the 45th week of 2012 (November 5-9). The Lange Steel (LGMI) Composite Price Index reached 149.6 points, representing a week-on-week increase of 0.72% and a year-on-year decrease of 13.20%. The LGMI Long Products Price Index stood at 166.0 points, marking a week-on-week increase of 0.03% and a year-on-year decrease of 15.31%. Meanwhile, the LGMI Sheet Price Index was 129.8 points, registering a week-on-week increase of 1.80% and a year-on-year decrease of 9.75%.

Data from the Lange Steel Information Research Center shows that the market prices of major steel products fluctuated slightly in the 45th week of 2012 (November 5-9). Compared to the previous week, there was a marginal increase in the number of rising varieties among standard products, while the number of falling varieties slightly decreased. Out of 44 monitored standard varieties across 17 categories in certain regions, 17 varieties increased, four decreased compared to the prior week; 14 varieties remained flat, increasing by one compared to the previous week; 13 varieties decreased, increasing by three compared to the previous week. Domestic iron and steel raw materials experienced mixed price movements, with iron ore and scrap markets remaining stable, coke prices rising by 70-150 yuan, and billet prices declining by 10-30 yuan.

2. The national steel stock market showed a slower decline this week. Nationwide steel inventories have been continuously decreasing, though the pace of decline for building materials slowed slightly, while the decline in sheet stocks accelerated somewhat. According to market monitoring by the Lange Steel Information Research Center, as of November 9th, the total steel society inventory in 29 key cities nationwide was 12,279,500 tons, a decrease of 217,900 tons from the previous week. By sub-category, national wire rod social inventories stood at 1,004,300 tons, down 2.29% from the previous week; rebar social inventories were 4,522,300 tons, up 0.12% from the previous week; Panluo social inventory was 264,500 tons, down 6.04% from the previous week; hot-rolled coil social inventory was 3,454,800 tons, down 3.95% from the previous week; cold-rolled coil social inventory was 1,585,900 tons, down 0.72% from the previous week; and plate social inventory was 1,447,800 tons, down 1.89% from the previous week.

3. The steel market remained volatile within a narrow range this week. In the 45th week of 2012 (November 5-9), the rebar and ferrous alloy markets experienced limited fluctuations, with market sentiment becoming increasingly cautious. The settlement price for the week fell by 36 points, yet in reality, the settlement price this week was only 5 points lower than the previous week, essentially remaining within the same price range. This week, the total open interest for the main contract was 1.07 million contracts, an increase of 123,000 contracts. The 1305 contract continued to expand for two consecutive weeks, indicating growing enthusiasm for thread futures, which also hinted at the potential emergence of medium-level prices.

4. Recent macroeconomic factors influencing steel prices:

In October, the non-manufacturing PMI rose by 1.8 percentage points. Data released by the National Bureau of Statistics Service Survey Center and the China Federation of Logistics and Purchasing on November 3rd showed that China's non-manufacturing business activity index reached 55.5% in October, up 1.8 percentage points from the previous quarter. Additionally, the new orders and employment indices remained stable, while the business activity expectations index surged significantly, reaching 63.4%. These figures indicate a positive trend in the non-manufacturing sector with accelerating growth.

The overall consumer price level increased by 1.7% year-on-year in October. Urban areas saw a 1.8% increase, while rural areas experienced a 1.5% rise. Food prices climbed by 1.8%, and non-food prices increased by 1.7%. Consumer goods prices went up by 1.5%, and service prices rose by 2.3%. From January to October, the cumulative consumer price level increased by 2.7% year-on-year. In October, the consumer price level dropped by 0.1% compared to the previous quarter. Cities experienced a 0.1% drop, while rural areas also saw a 0.1% decrease. Food prices fell by 0.8%, while non-food prices rose by 0.3%. Consumer goods prices declined by 0.2%, whereas service prices increased by 0.2%.

The national industrial producer's factory price fell by 2.8% year-on-year in October. Data from the National Bureau of Statistics showed that industrial producer prices fell by 2.8% year-on-year and 0.2% month-on-month. Industrial producer purchase prices decreased by 3.3% year-on-year and rose by 0.1% month-on-month. From January to October, industrial producer ex-factory prices fell by 1.6% year-on-year, and purchase prices decreased by 1.7% year-on-year. Within ex-factory prices, the means of production fell by 3.7% year-on-year, including a 6.4% drop in mining industry prices, a 3.4% decline in raw material industry prices, and a 3.5% fall in processing industry prices. Living materials prices rose by 0.2% year-on-year, with food prices increasing by 0.3%, clothing by 1.6%, general commodities by 0.5%, and durable consumer goods falling by 1.0%. Among purchase prices, ferrous materials fell by 11.4% year-on-year, chemical raw materials by 5.7%, non-ferrous metal materials and wires by 3.1%, textile raw materials by 2.2%, and fuel power by 1.5%.

Fixed asset investment grew by 20.7% year-on-year from January to October. Data from the National Bureau of Statistics indicated that fixed asset investment (excluding rural households) reached 29,254.2 billion yuan from January to October, representing a nominal year-on-year increase of 20.7%, 0.2 percentage points higher than the growth rate for the first nine months. On a month-to-month basis, fixed asset investment (excluding rural households) increased by 1.94% in October.

By sub-sector, from January to October, investment in the primary industry was 743.7 billion yuan, up 32.3% year-on-year, 0.1 percentage points higher than the growth rate for the first nine months; investment in the secondary industry was 1,287.5 billion yuan, up 21.9%, 0.5 percentage points lower than the growth rate for the first nine months; investment in the tertiary industry reached 15,631.9 billion yuan, up 20.1%, 0.7 percentage points higher than the growth rate for the first nine months. Within the secondary industry, industrial investment was 1,258.3 billion yuan, up 21.9%, 0.6 percentage points lower than the growth rate for the first nine months. Among these, mining industry investment was 1,005.7 billion yuan, up 14.7%, 2.7 percentage points lower than the growth rate for the first nine months; manufacturing investment was 1,018.8 billion yuan, up 23.1%, 0.4 percentage points lower than the growth rate for the first nine months; investment in electricity, heat, gas, and water production and supply was 1,343.7 billion yuan, up 18.6%, 0.5 percentage points lower than the growth rate for the first nine months.

Industrial added value above designated size increased by 9.6% year-on-year in October. Data from the National Bureau of Statistics showed that industrial enterprises above designated size registered a year-on-year increase of 9.6% in their added value in October (the growth rate excluding price factors), which was 0.4 percentage points faster than in September. On a month-to-month basis, the added value of industries above designated size increased by 0.81% from the previous month in October. From January to October, the industrial added value of above-scale industries increased by 10.0% year-on-year.

By sub-sector, in October, the added value of all 41 major industrial sectors increased year-on-year. Textile industry growth was 11.9%, chemical raw materials and chemical products manufacturing growth was 11.9%, non-metallic mineral products industry growth was 11.0%, ferrous metal smelting and rolling processing industry growth was 12.6%, general equipment manufacturing industry growth was 7.1%, automobile manufacturing industry growth was 5.9%, railway, ship, aerospace, and other transportation equipment manufacturing growth was 6.1%, electrical machinery and equipment manufacturing growth was 7.9%, computer, communication, and other electronic equipment manufacturing growth was 10.1%, and electricity and heat production and supply industry growth was 4.7%.

Industry news:

Shandong Province is restructuring its steel industry by consolidating steel companies into six major groups by 2015. As a pilot region for structural adjustments in the steel industry, Shandong plans to reduce the number of steel enterprises from 21 to six major steel groups by 2015. Total steel production capacity will be adjusted from the current 63.07 million tons to 50 million tons, with an increase in coastal steel production to 43%. Enterprise mergers and acquisitions are a critical component of Shandong's steel structure adjustment pilot. On November 1st, the "Shandong Iron & Steel (Group) Co., Ltd. Merger and Reorganization Plan" was published. In addition to the core Shandong Steel Group, five regional steel enterprise groups will also be established in Zibo, Weifang, Laiwu, Linyi, and Binzhou.

Crude steel production fell by 5.4% in the last quarter of October. Statistics from the China Iron and Steel Association showed that the average daily output of crude steel for major and medium-sized enterprises in late October was 15.195 million tons, a decrease of 86,600 tons from the previous month and a 5.4% decrease from the previous month. In the second half of October, the country's crude steel production was estimated to be 21.183 million tons, with an average daily output of 1.926 million tons, a decrease of 73,000 tons from the middle of the month and a 3.7% decrease from the previous month. The data also showed that the average daily output of crude steel in October was 1.658 million tons, an increase of 1.4% from September.

The Ministry of Commerce decided to impose anti-dumping duties on imports of certain high-performance stainless steel seamless pipes originating from the European Union and Japan. On November 8th, the Ministry of Commerce issued Bulletin No. 72 of 2012, announcing the final results of the anti-dumping investigation into certain high-performance stainless steel seamless pipes. Starting November 9, 2012, anti-dumping duties of 9.2% to 14.4% will be imposed on imports of these products originating from the EU and Japan, valid for five years. After investigation, the investigating authority concluded that during the investigation period, there was dumping of the product under investigation, causing substantial damage to the relevant high-performance stainless steel seamless pipe industry in China, with a causal link between dumping and substantial damage. Therefore, the Ministry of Commerce decided to impose anti-dumping duties on the above products originating from the EU and Japan starting November 9, 2012. The Ministry of Commerce initiated an anti-dumping investigation into the aforementioned products on September 8, 2011, and issued a preliminary ruling on May 8, 2012, confirming the existence of dumping in the investigated products.

The rebar main contract for the 9th session closed up, with the main contract rising by 0.52%. The rebar main 1305 contract opened at 3,640 yuan/ton on the morning of the 9th, showing an intraday downward trend throughout the day. The lowest price of the day was 3,628 yuan/ton, and the highest was 3,673 yuan/ton, closing at 3,640 yuan/ton. The settlement price on the previous trading day (8th) rose by 19 yuan/ton, with a trading volume of 2,328,602 lots and open interest totaling 1,070,130 contracts, an increase of 10,862 contracts.

Downstream demand:

Fixed asset investment in railways decreased by 0.9% month-on-month in October. Statistics from the Ministry of Railways showed that from January to October, national railway fixed asset investment totaled 425.169 billion yuan, a year-on-year decrease of 0.9%. Among these, national railway infrastructure investment reached 361.816 billion yuan, a year-on-year decrease of 1.5%.

Statistics from the Ministry of Housing and Urban Development showed that from January to October, a total of 7.22 million sets of new urban housing security projects were completed, with approximately 505 million units finished, and an investment of 1,080 billion yuan was completed. According to the plan, this year, more than 7 million sets of urban housing projects will be newly built in cities, with approximately 5 million units planned for completion.

From January to October, national sales of home appliances to rural areas exceeded 60 million units. Statistics from the Ministry of Commerce showed that from January to October, 65.22 million units of home appliances were sold nationwide (excluding Shandong, Henan, Sichuan, and Qingdao), achieving sales of 175.24 billion yuan, representing year-on-year increases of 23.5% and 18.8%, respectively. In October alone, the country sold 7.91 million home appliances to rural areas, achieving sales of 21.38 billion yuan, representing year-on-year increases of 27.5% and 26.0%. As of the end of October 2012, the country had sold 283 million home appliances to rural areas, achieving sales of 681.1 billion yuan.

From January to October, national real estate development investment increased by 15.4% year-on-year. Data from the National Bureau of Statistics showed that from January to October, total real estate development investment in the country reached 5,769,900 million yuan, an increase of 15.4% year-on-year, the same growth rate as from January to September. Among these, residential investment was 3,974.0 billion yuan, an increase of 10.8%, with a growth rate increase of 0.3 percentage points, accounting for 68.9% of total real estate development investment.

From January to October, the housing construction area of real estate development enterprises was 538.149 million square meters, an increase of 13.3% year-on-year, with a growth rate 0.7 percentage points lower than that of the first nine months. Among these, the residential construction area was 403.203 million square meters, an increase of 10.9%. The area of new housing starts was 1,476.92 million square meters, a decrease of 8.5%, with a decline 0.1 percentage points narrower than that of January to September. Among these, the newly started residential area was 1,083.96 million square meters, a decrease of 12.7%. The completed building area was 58.317 million square meters, an increase of 17.3%, with a growth rate increase of 0.9%. Among these, the residential building completed area was 476.92 million square meters, an increase of 17.1%.

Hovercraft Fan Blades,Plastic Fan Impeller,Fan Blades For Hovercraft,Axial Fan Blades For Airboat

Changzhou Keyleader Fan Technology Co. Ltd. , https://www.keyleaderfan.com